Scientists across the globe have made it clear that greenhouse gas (GHG) emissions have been causing major changes to climates all over the world. While there are a number of ways that individuals can reduce their carbon emissions, it’s been noted that a majority of the GHG emissions causing climate change are being emitted by enterprise organizations and corporations.

For organizations that are seeking to reduce their GHG output, it’s important that companies measure all three types of emissions and understand the difference between Scopes 1, 2, and 3 emissions in order to pinpoint exactly where the biggest reduction can be made to carbon emissions.

This article will answer what Scope 1, 2, and 3, emissions are as well as where organizational reuse fits into the broader picture.

Scope 1, 2, and 3 emissions

Scope 1, 2, and 3 emissions are terms used to describe the different types of GHG emissions that encompass an organization’s environmental impact. These scopes were determined by a partnership of organizations called the Greenhouse Gas Protocol. This partnership consists of a collective of businesses, NGOs, governments, and other stakeholders. It was launched in 1993 with the mission to develop internationally accepted GHG accounting and reporting standards and tools, and to promote their adoption in order to achieve a low-emissions economy worldwide.

This organization has laid the foundation for defining, reporting, and tackling GHG emissions based on three scopes. According to the GHG Protocol corporate standard, Scope 1 and 2 emissions are mandatory to report. Scope 3 emissions reporting is voluntary due to how difficult it is to monitor. Organizations successful in reporting all three scopes of emissions will gain a sustainable competitive advantage in their industry, but they would be the exception rather than the norm. Most organizations struggle greatly with reporting on all three scopes due to underlying complexities in the reporting process and product life cycles, – or due to a lack of tools altogether. Let’s look at the different scopes and learn how they work to define an organization’s total GHG footprint.

Scope 1 emissions

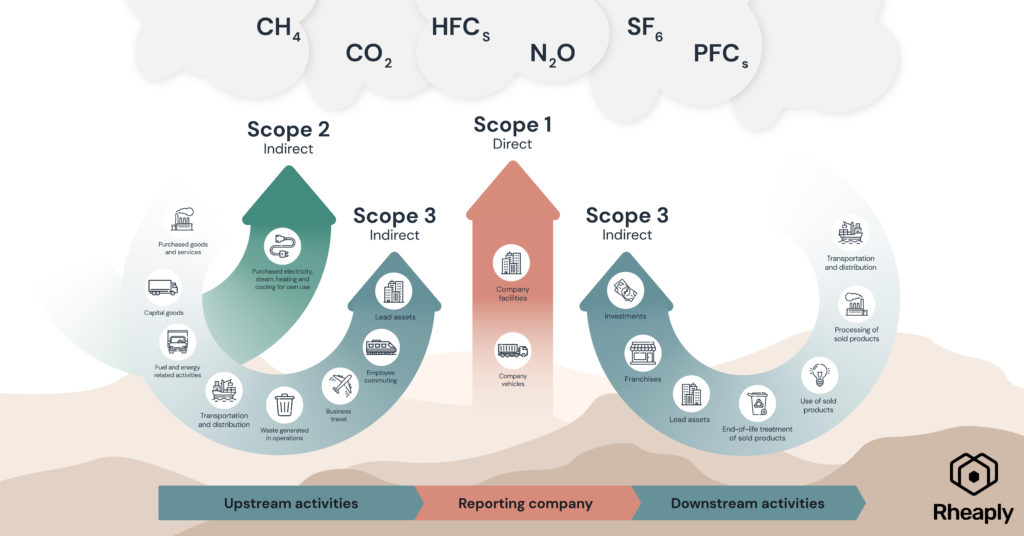

Scope 1 emissions are direct emissions from company-owned and controlled resources. These are GHG emissions that are released into the atmosphere as a result of either stationary combustion (burning fuel for heating sources and other operations) or mobile combustion (burning fuel in fleet cars, vans, or trucks). Scope 1 emissions also include fugitive emissions from refrigeration or air conditioning units which are more dangerous than CO2. The final contributor of Scope 1 emissions comes from process emissions which are produced during industrial processes and manufacturing.

Scope 1 emissions are mandatory to report and often the easiest to calculate since they are directly related to an organization’s business function and methods.

Scope 2 emissions

Scope 2 emissions are owned, indirect emissions from the generation of energy from a utility provider. These GHG emissions are released into the atmosphere from the consumption of purchased electricity among other utilities. This scope encompasses the electricity consumed by the end-user.

Scope 2 emissions are mandatory to report and can be easily calculated based on the end-user’s overall electricity consumption from fossil fuel sources. Strategies to reduce Scope 2 emissions are a powerful mechanism for the private sector to push for impactful change in the power sector’s generation portfolio, which can be especially important in the absence of clear and consistent US policy.

Scope 3 emissions

Scope 3 emissions are the most wide-spread indirect emissions which are not directly owned by your organization. These occur in the value chain of the company, including both upstream and downstream emissions linked to the organization’s operations. The GHG Protocol has separated these emissions into 15 categories. Scope 3 is often called the “everything else” scope of emissions.

Scope 3 emissions are not part of mandatory reporting due to the difficulty in measurement. However, this scope of emissions also typically represents the most significant opportunities for improvement among corporations, with product life cycles encompassing the majority of an organization’s total GHG emissions.

Unfortunately it’s often an opportunity wasted because the complexity of upstream suppliers and downstream consumers/users make it nearly impossible for organizations to compile the necessary data to complete an accurate Scope 3 emissions profile.

Scope 3 emissions examples

Upstream activities that feed into Scope 3 emissions fall into several categories.

For many organizations, travel is one of the most important to report. Business travel through airplanes, trains, taxis, or private vehicles should be reported as well as employee commuting. These can be reduced through public transportation and remote work policies.

Emissions associated with waste sent to landfills and wastewater treatment are categorized under Scope 3 emissions as well. Waste disposal can also emit other GHGs such as methane and nitrous oxide which cause greater damage than CO2 emissions. We will discuss in a later section how reuse can help reduce this category of Scope 3 emissions.

The purchased goods and services category includes all the upstream emissions from the production of goods and services purchased by the organizations. These are different from materials, components or parts used for production by the company and instead focus on non-production-related products like office furniture, fixtures, and IT equipment.

Transportation and distribution emissions occur in upstream and downstream elements of an organization’s value chain where anything is being moved by land, sea, or air as well as third-party warehousing.

Fuel and energy-related emissions are a result of the production of fuel and energy purchased and consumed by the reporting organization that is not included in Scope 1 and 2 categories.

Capital goods are final products used by a company in its operations and includes buildings, vehicles, and machinery. Extending the life of capital goods related to buildings through reuse will be discussed in a later section.

Downstream activities covered under Scope 3 are most notably related to investments, franchises, and leased assets owned by a reporting organization. The use of products sold to consumers and the end-of-life-treatment of products sold to consumers is also included under Scope 3. Companies must assess how the products they produce emit GHG emissions and/or are disposed of. This encourages companies to design products that encourage reuse, repair, or recycling versus being sent to a landfill for disposal.

Rheaply as a Scope 3 solution

While there is no direct solution for reducing all Scope 3 emissions along an organization’s value chain, adopting reuse practices reduces Scope 3 emissions over time.

Purchased goods and services

Reduce the amount of production goods (e.g. materials) and non-production goods (e.g. furniture & fixtures) purchased over time by supporting asset reuse. For some organizations such as construction or manufacturing, providing access to reused (i.e. lower-carbon) materials to produce goods or perform services is also relevant.

Capital goods

Reduce the amount of capital goods (e.g. machinery, vehicles, buildings used for surplus storage) purchased over time by supporting asset reuse. Support in lowering construction impacts through building materials reuse (for companies involved in the construction of their own facilities).

Waste generated in operations

Reduce the tonnage of goods sent to landfill by supporting asset reuse, recycling and other recovery efforts. Rheaply creates non-landfill (i.e. lower-emissions) disposition outcomes through timely connections to ecosystem recycling and remanufacturing partners.

End-of-life treatment of sold products

Manufacturers should support the recirculation of their goods to reduce tonnage of sold products sent to landfill after customer use. Additionally, they should support non-landfill (i.e. lower-emissions) disposition methods for sold goods through connections to ecosystem disposition partners.

Scope 3 reporting

Rheaply’s estimated embodied carbon avoided reporting feature provides a solution for determining your GHG impact through reuse of an organization’s materials and within their manufacturing processes. This report can help employees better understand and gain insight into the environmental impact of resource exchange within their organizations.